C-suite

C-suite · Founders post-exit

Concentration, liquidity, and planning explainers written for leaders who already run complex businesses.

Net Pay Estimator

Illustrative$140,125

Federal

$52,500

State

$20,868

FICA

43%

Eff. Rate

Illustrative estimate only — not tax advice. Uses simplified 2025 federal brackets and estimated state effective rates. Verify with a licensed CPA or tax professional.

40%+

C-suite comp in equity on average

LTIP

Vesting timing is a tax event

$10M+

Estate exposure threshold common

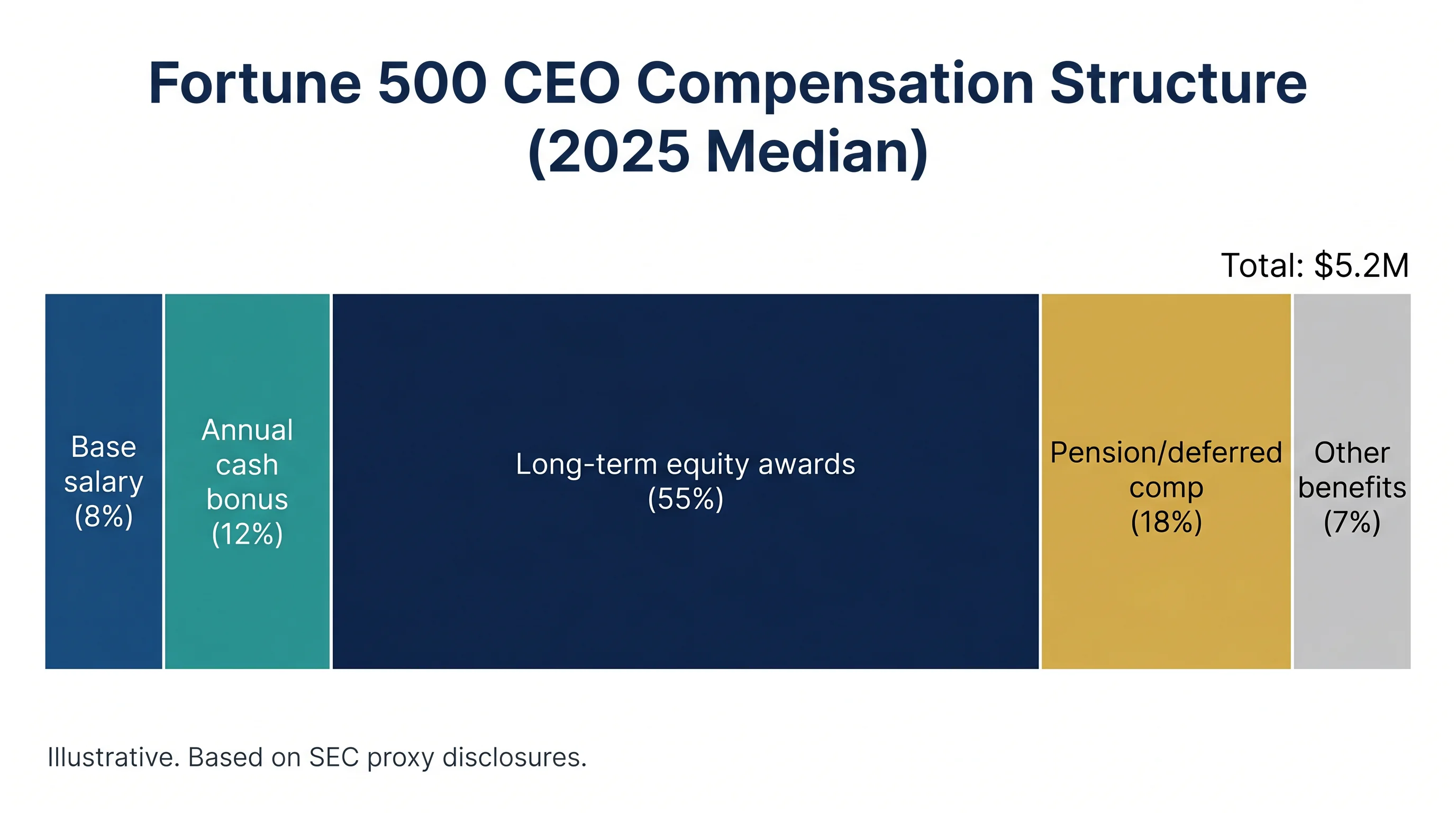

Fortune 500 executive compensation structure — Illustrative. Not financial advice.

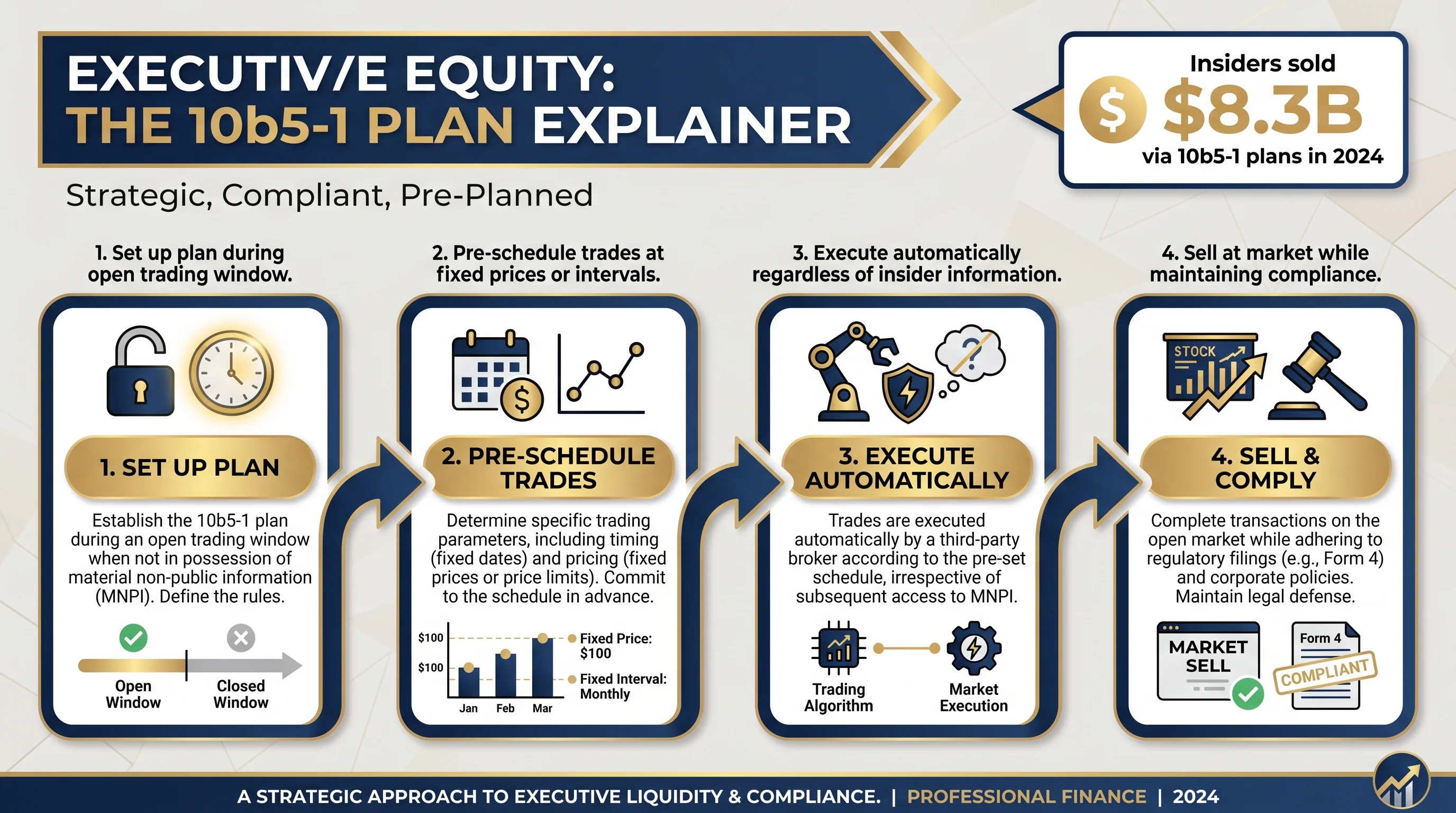

10b5-1 plan — 4-step process for compliant insider equity sales — Illustrative.

What We Cover

RSUs, options, 10b5-1 plans, and blackout period strategy

NQDC tax arbitrage, distribution scheduling, counterparty risk

AMT planning, SALT cap optimization, and bonus timing

GRATs, IDGTs, family limited partnerships for wealth transfer

SERP, split-dollar life, executive health benefit optimization

Executive Wealth Complexity

A 10b5-1 plan, deferred compensation election, and NQSO exercise all interact with each other and with your tax bracket. Getting the sequencing wrong during a high-liquidity year can cost more than a year of advisor fees.

Explore executive comp tools

Practical guides and scenario tools for clevelfinance professionals — every article ships with a calculator or scenario box.

clevelfinancial.com targets leaders with lumpy income, material equity events, and reputational sensitivity. Content covers 10b5-1 planning literacy, diversification without signaling, private banking jargon translation, and family office-lite workflows. Calculators speak in vest calendars, blackout windows, and concentration metrics. Tone is peer-level, not coachy.

C-suite · Founders post-exit

VP+ leaders · PE operating partners evaluating personal side

Board members managing personal and fiduciary tension

In practice

Help executives and senior leaders navigate equity, concentration, deferred comp, and personal balance sheets alongside board-level demands—monetized as ads + membership with optional $99 advisory for complex structuring. clevelfinancial.com targets leaders with lumpy income, material equity events, and reputational sensitivity. Content covers 10b5-1 planning literacy, diversification without signaling, private banki

Featured tools

clevelfinancial.com readers get calculators with assumptions, language, and examples native to their career — purpose-built for this desk, not relabeled consumer-finance tools.

Interactive

clevelfinancial.com readers get calculators with assumptions, language, and examples native to their career — purpose-built for this desk, not relabeled consumer-finance tools.

Future value

$1,185,264

Projected ending balance under the current compounding path.

Your contributions

$460,000

Starting capital plus every monthly contribution.

Investment growth

$725,264

The share created by compounding instead of deposits.

Output path

The line updates immediately as you change the assumptions.

Year 0 to Year 20

Interactive

clevelfinancial.com readers get calculators with assumptions, language, and examples native to their career — purpose-built for this desk, not relabeled consumer-finance tools.

Enter current and target weights. The model normalizes them to 100% and flags any sleeve that sits outside your drift band.

equities

fixed Income

alternatives

cash

Largest sleeve

55%

Anything too dominant deserves extra governance.

Effective sleeves

2.6

A lower value means the portfolio behaves like fewer real bets.

Concentration score

0.39

Herfindahl-style concentration across the current weights.

equities

Current 55% vs target 60%

Drift: -5%. Keep this sleeve within +/-5% to stay inside the current policy.

fixed Income

Current 25% vs target 20%

Drift: 5%. Keep this sleeve within +/-5% to stay inside the current policy.

alternatives

Current 10% vs target 10%

Drift: 0%. Keep this sleeve within +/-5% to stay inside the current policy.

cash

Current 10% vs target 10%

Drift: 0%. Keep this sleeve within +/-5% to stay inside the current policy.

Interactive

clevelfinancial.com readers get calculators with assumptions, language, and examples native to their career — purpose-built for this desk, not relabeled consumer-finance tools.

Nominal balance

$3M

Raw dollars at the retirement start date.

Today's dollars

$2M

Inflation-adjusted view of the same future balance.

4% rule estimate

$130K

A quick annual draw estimate before tax planning.

Output path

The line updates immediately as you change the assumptions.

42 to 65

Sustainable real income

$112K

Approximate annual spending in today's dollars if the portfolio must last through retirement.

Membership

Reader

$0

Member

$4.99/month

Optional advisory

$99 intake

FAQ

Executive-grade personal finance intelligence that respects calendar density and confidentiality norms.

No. Materials are general education and illustration. Decisions involving securities, taxes, or planning should involve your own licensed professionals.

Remove ads and keep sessions focused for $4.99/month; premium modules roll in over time per roadmap.

Licensing disclosures; Niche-specific limitations; Privacy

Practical guides and scenario tools for clevelfinance professionals — every article ships with a calculator or scenario box.

Contact

Standalone executive brand. Its design, voice, and content focus belong to leadership comp, equity events, and governance — not household finance or operator capital.

Equity compensation, deferred comp timing, golden handcuff analysis, and board governance considerations all interact. Fenul Wealth integrates every dimension into one clear plan.

Opens fenulwealthmanagement.com · General education only · No fiduciary relationship formed on this page